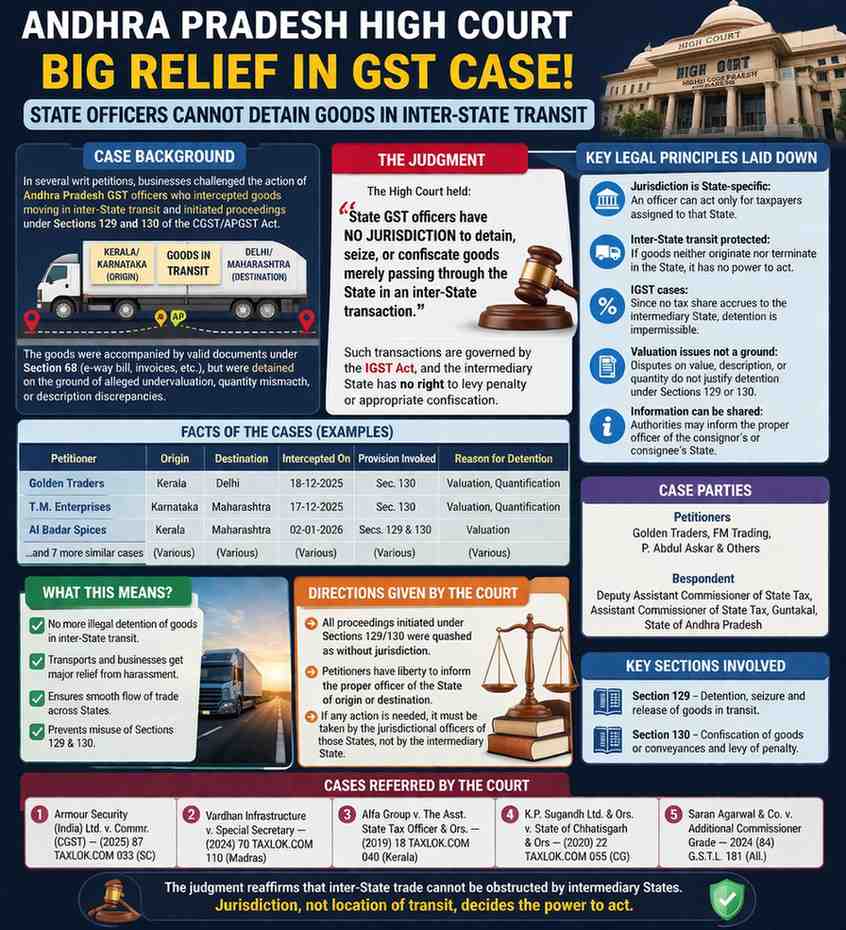

???? GST Judgement Explained in Hindi – Andhra Pradesh High Court (Golden Traders Case)

????️ Case Overview

Andhra Pradesh High Court ने एक महत्वपूर्ण निर्णय दिया है जिसमें यह स्पष्ट किया गया कि Inter-State Transit में goods को बीच वाला State रोक नहीं सकता।

- Court: Andhra Pradesh High Court

- Date: 01 April 2026

- Case: Golden Traders & Others vs State Tax Authorities

- Key Issue: क्या कोई intermediary State transit goods को detain कर सकता है?

⚖️ Background of the Case

इस केस में goods एक State से दूसरे State (जैसे Kerala से Delhi/Maharashtra) जा रहे थे और केवल Andhra Pradesh से गुजर रहे थे।

State GST अधिकारियों ने:

- Goods को detain किया

- Section 129 और 130 के तहत कार्रवाई की

- Reason बताया: valuation mismatch और quantity discrepancy

???? सवाल यह था कि क्या ऐसा detention वैध है?

???? Arguments by Both Sides

???? Taxpayer (Assessee) का पक्ष:

- यह IGST (Inter-State Supply) का मामला है

- Andhra Pradesh का इससे कोई संबंध नहीं

- इसलिए State GST अधिकारी को jurisdiction नहीं है

???? Department का पक्ष:

- Section 129 और 130 के तहत action लिया जा सकता है

- Valuation और mismatch detention का आधार हो सकता है

⚖️ High Court Judgment (Key Findings)

✅ 1. Inter-State Transit में State का अधिकार नहीं

अगर goods एक State से दूसरे State जा रहे हैं और केवल बीच से गुजर रहे हैं, तो intermediary State उन्हें detain या confiscate नहीं कर सकता।

✅ 2. IGST मामलों में अधिकार सीमित

IGST मामलों में tax collection Centre द्वारा किया जाता है, इसलिए बीच वाले State को कोई अधिकार नहीं है penalty या confiscation का।

✅ 3. Section 129/130 का misuse रोका गया

Court ने कहा कि ये provisions केवल तब लागू होंगे जब clear tax evasion का intent हो।

???? केवल valuation dispute पर detention नहीं हो सकता।

✅ 4. Valuation Issue = No Detention

अगर invoice और e-way bill सही हैं और केवल price difference है, तो goods को रोका नहीं जा सकता।

✅ 5. Proper Officer की सीमाएं

हर GST officer की jurisdiction सीमित होती है।

Cross-empowerment का मतलब unlimited power नहीं है।

✅ 6. Discrepancy होने पर क्या करें?

अगर कोई discrepancy मिलती है तो:

- State officer खुद action नहीं ले सकता

- केवल information forward कर सकता है

- Consignor State को

- Consignee State को

???? Final Conclusions by Court

- State officer action तभी ले सकता है जब taxpayer उसी State को allotted हो

- Intra-state cases में action valid है

- IGST में action तभी valid है जब उस State को tax share मिले

- Inter-State transit (third State case) में कोई action नहीं ले सकता

- केवल information forward की जा सकती है

???? Practical Impact on Businesses

???? Benefits:

- Transit में unnecessary detention खत्म

- Harassment कम होगा

- Business operations smooth होंगे

⚠️ Department Limitations:

- Arbitrary detention नहीं कर सकते

- Valuation के नाम पर goods नहीं रोक सकते

???? Example for Better Understanding

मान लीजिए goods Kerala से Delhi जा रहे हैं और Andhra Pradesh से गुजर रहे हैं:

- ❌ Andhra Pradesh goods नहीं रोक सकता

- ❌ Penalty नहीं लगा सकता

- ✔️ केवल report कर सकता है

???? Final Conclusion

Inter-State transit में कोई भी intermediary State Section 129/130 के तहत goods को detain या confiscate नहीं कर सकता।

Comments (0)

Abhi tak koi comment nahi. Pehle comment karein!