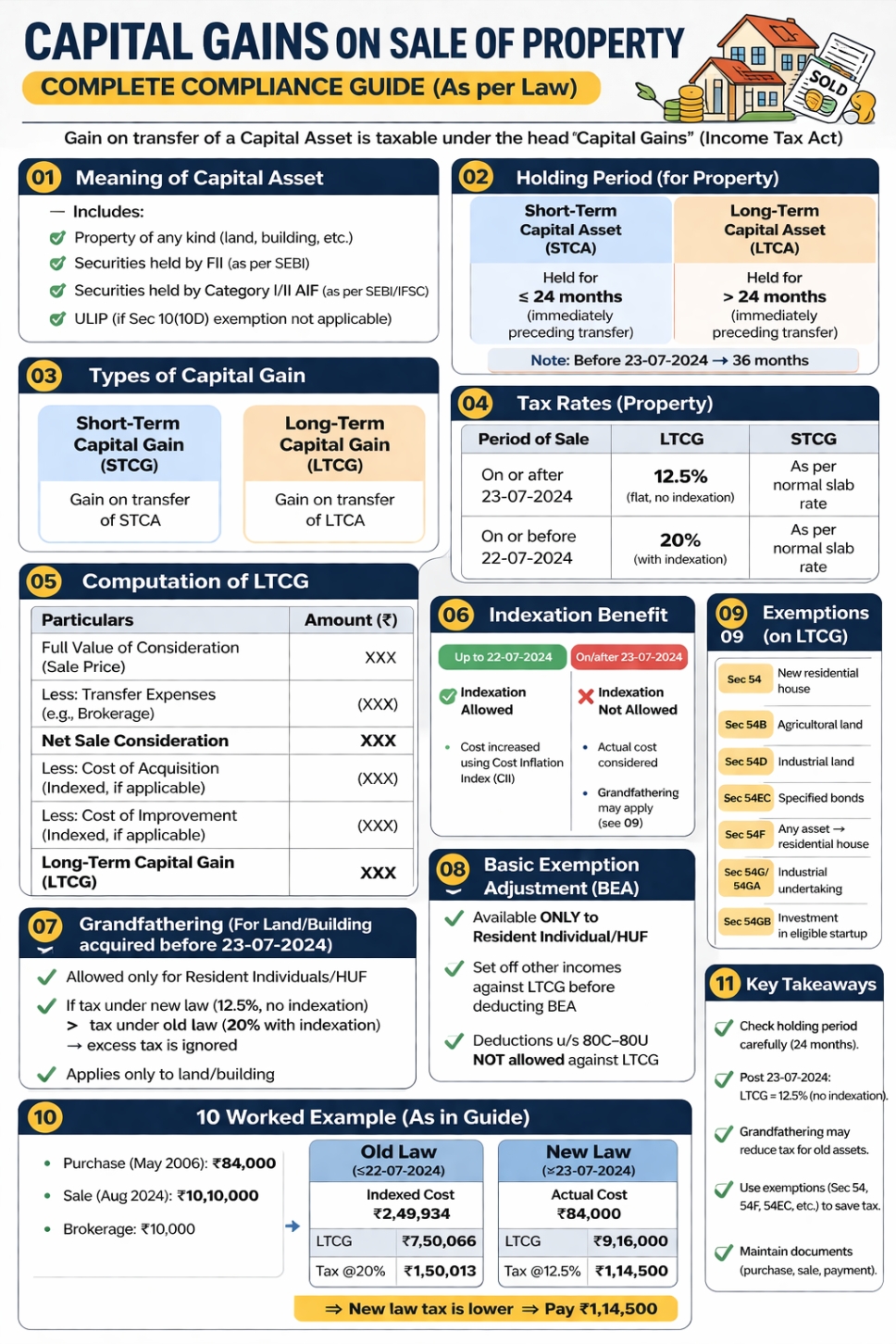

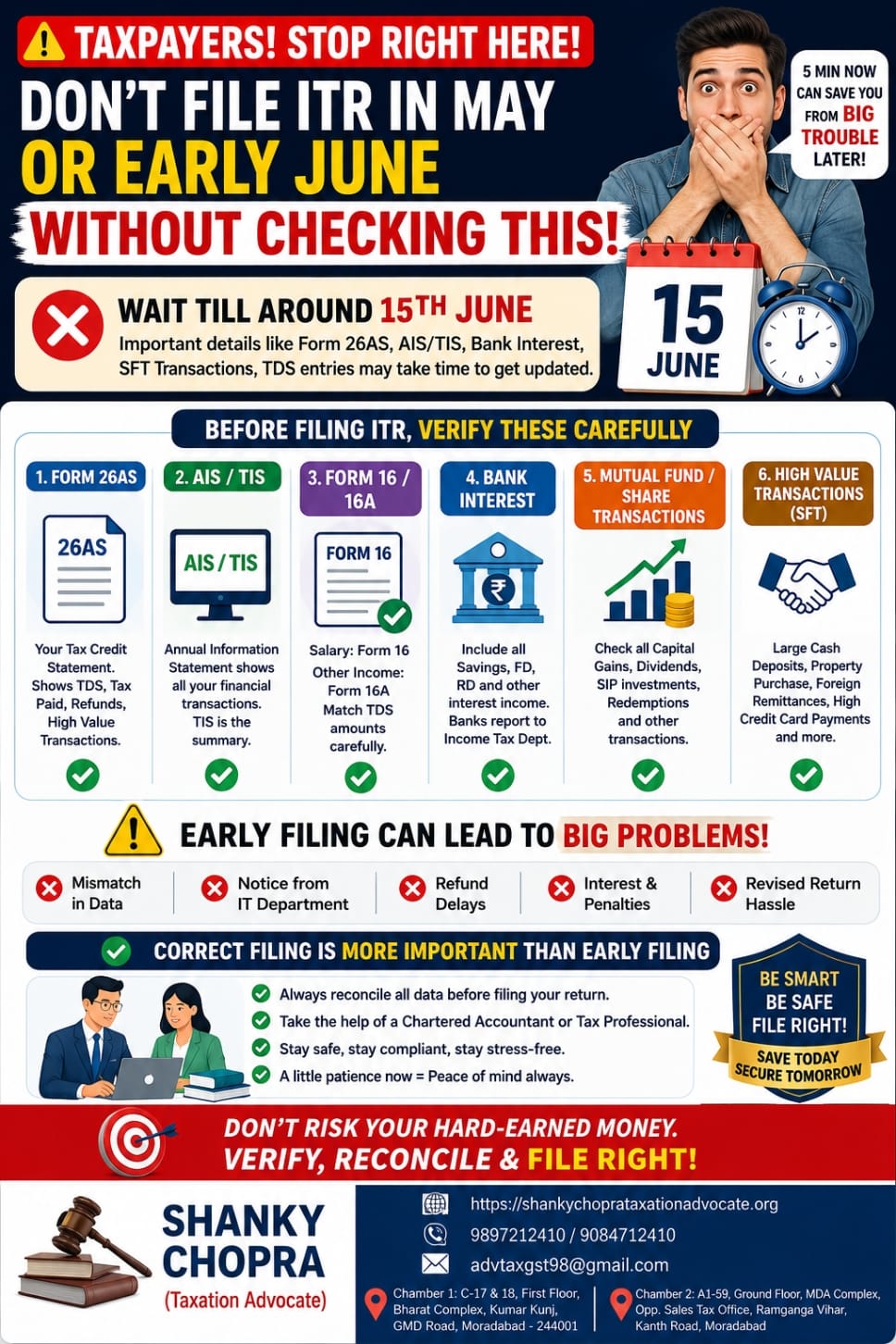

# Capital Gains on Property (2026): Complete Guide to LTCG, STCG & Tax Calculation in India

# Introduction

When you sell a property and earn a profit, that profit is called Capital Gain and is taxable under the Income Tax Act. Understanding how LTCG (Long-Term Capital Gain) and STCG (Short-Term Capital Gain) work is essential to avoid excess tax and plan legally.

This guide explains latest rules after 23 July 2024, tax rates, calculation method, and exemptions.

# What is Capital Gain?

Capital Gain is the profit earned on transfer (sale) of a capital asset such as:

- Land

- Residential house

- Commercial property

- Securities (in some cases)

# It is taxed under the head “Capital Gains”.

# What is a Capital Asset?

A capital asset includes:

- Property of any kind (land/building)

- Securities held by FII/AIF

- Certain ULIPs (where exemption u/s 10(10D) is not available)

# Holding Period: STCG vs LTCG

# Short-Term Capital Asset (STCA)

- Held for 24 months or less

- # Gain = STCG

# Long-Term Capital Asset (LTCA)

- Held for more than 24 months

- # Gain = LTCG

# Important Note:

- Before 23-07-2024, the limit was 36 months

# Types of Capital Gains

# Short-Term Capital Gain (STCG)

- Gain from short-term asset

- Taxed at normal income tax slab rates

# Long-Term Capital Gain (LTCG)

- Gain from long-term asset

- Special tax rates apply

# Tax Rates on Property (Latest 2026)

# LTCG Tax

- On or after 23-07-2024 → 12.5% (No indexation)

- On or before 22-07-2024 → 20% (with indexation)

# STCG Tax

- Taxed as per normal income tax slab

# How to Calculate Capital Gains

# LTCG Calculation Formula

Step 1: Full Sale Value

Step 2: Less: Transfer Expenses (brokerage, etc.)

Step 3: Net Sale Consideration

Step 4: Less: Cost of Acquisition

Step 5: Less: Cost of Improvement

# Result = Capital Gain

# Indexation Rule (Major Change)

# After 23-07-2024

- No indexation benefit

# Before 23-07-2024

- Cost adjusted using Cost Inflation Index (CII)

# Grandfathering Provision

Applicable when:

- Property acquired before 23-07-2024

- Only for Resident Individual / HUF

- Only for land or building

# If tax under new rule (12.5%) is higher than old rule (20% with indexation),

then excess tax will not be charged

# Example (Important for Understanding)

- Purchase (May 2006): ₹84,000

- Sale (Aug 2024): ₹10,10,000

- Brokerage: ₹10,000

# Old Method (with indexation)

- LTCG: ₹7,50,066

- Tax @20% = ₹1,50,013

# New Method (without indexation)

- LTCG: ₹9,16,000

- Tax @12.5% = ₹1,14,500

# Conclusion: New method is better (lower tax)

# Basic Exemption Adjustment

✔ Allowed only to Resident Individual / HUF

✔ First adjust other income, then LTCG

# No deduction allowed under Section 80C to 80U against LTCG

# Exemptions to Save Capital Gains Tax

You can save tax by reinvesting under:

- Section 54 → Residential house

- Section 54B → Agricultural land

- Section 54D → Industrial land/building

- Section 54EC → Specified bonds

- Section 54F → Investment in house property

- Section 54G / 54GA → Industrial shifting

- Section 54GB → Startup investment

✅ Key Takeaways

✔ Capital Gain depends on holding period (24 months rule)

✔ LTCG tax is 12.5% after 23-07-2024 (no indexation)

✔ STCG taxed as per normal slab

✔ Use Section 54 series to save tax

✔ Compare old vs new method before filing

Comments (0)

Abhi tak koi comment nahi. Pehle comment karein!