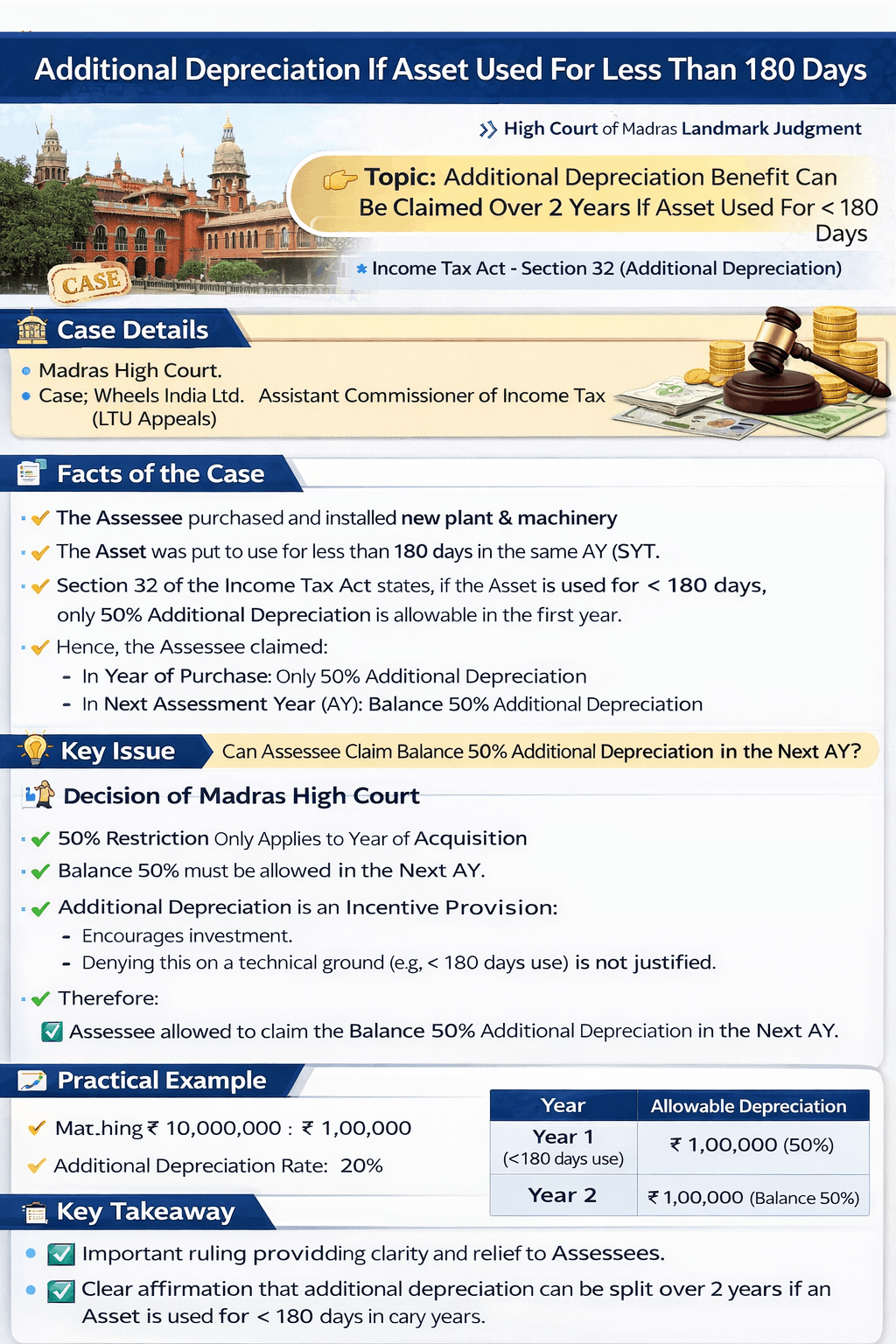

# Additional Depreciation Allowed in 2 Years – Madras High Court Relief

# Introduction

A major relief has been provided to taxpayers by the Madras High Court regarding the claim of additional depreciation under Section 32 of the Income Tax Act.

This ruling clarifies that even if a new asset is used for less than 180 days, the taxpayer is still eligible to claim 100% additional depreciation, though it may be spread across two financial years.

# Case Overview

- Case Name: Wheels India Ltd. vs ACIT (Appeals)

- Court: Madras High Court

- Date: 02 March 2026

The case revolved around whether the remaining 50% additional depreciation can be claimed in the subsequent year if the asset was used for less than 180 days in the year of purchase.

# Legal Provision – Section 32

As per Section 32(1)(iia) of the Income Tax Act:

- Additional depreciation is allowed on new Plant & Machinery

- If the asset is used for less than 180 days, only 50% depreciation is allowed in the first year

# But the law was unclear earlier about the remaining 50%

# Issue in Dispute

The main question was:

Can the balance 50% additional depreciation be claimed in the next financial year?

The Assessing Officer (AO) denied this claim, stating that once restricted in the first year, the remaining benefit cannot be carried forward.

# High Court Judgment

The Madras High Court ruled in favor of the taxpayer and held:

# Key Findings:

- The restriction of 50% applies only in the year of acquisition

- The remaining 50% must be allowed in the subsequent year

- Additional depreciation is a beneficial provision

- It should be interpreted to promote investment, not restrict it

# Practical Example

Let’s understand with an example:

- Cost of Machinery: ₹10,00,000

- Additional Depreciation @20% = ₹2,00,000

YearDepreciation AllowedYear 1 (<180 days use)₹1,00,000 (50%)Year 2₹1,00,000 (Remaining 50%)

# Total benefit = 100% allowed (in 2 years)

# Why This Judgment is Important

✔️ Prevents loss of legitimate tax benefits

✔️ Encourages businesses to invest in new machinery

✔️ Clarifies long-standing confusion in tax assessments

✔️ Supports taxpayer-friendly interpretation of law

# Expert Insight

This ruling reinforces the principle that tax incentives should be fully available to taxpayers and should not be denied due to technical limitations like usage duration.

# Conclusion

The Madras High Court has clearly established that:

# Additional Depreciation cannot be denied — only deferred

This is a significant relief for businesses, especially those making investments toward the end of the financial year.

Comments (0)

Abhi tak koi comment nahi. Pehle comment karein!