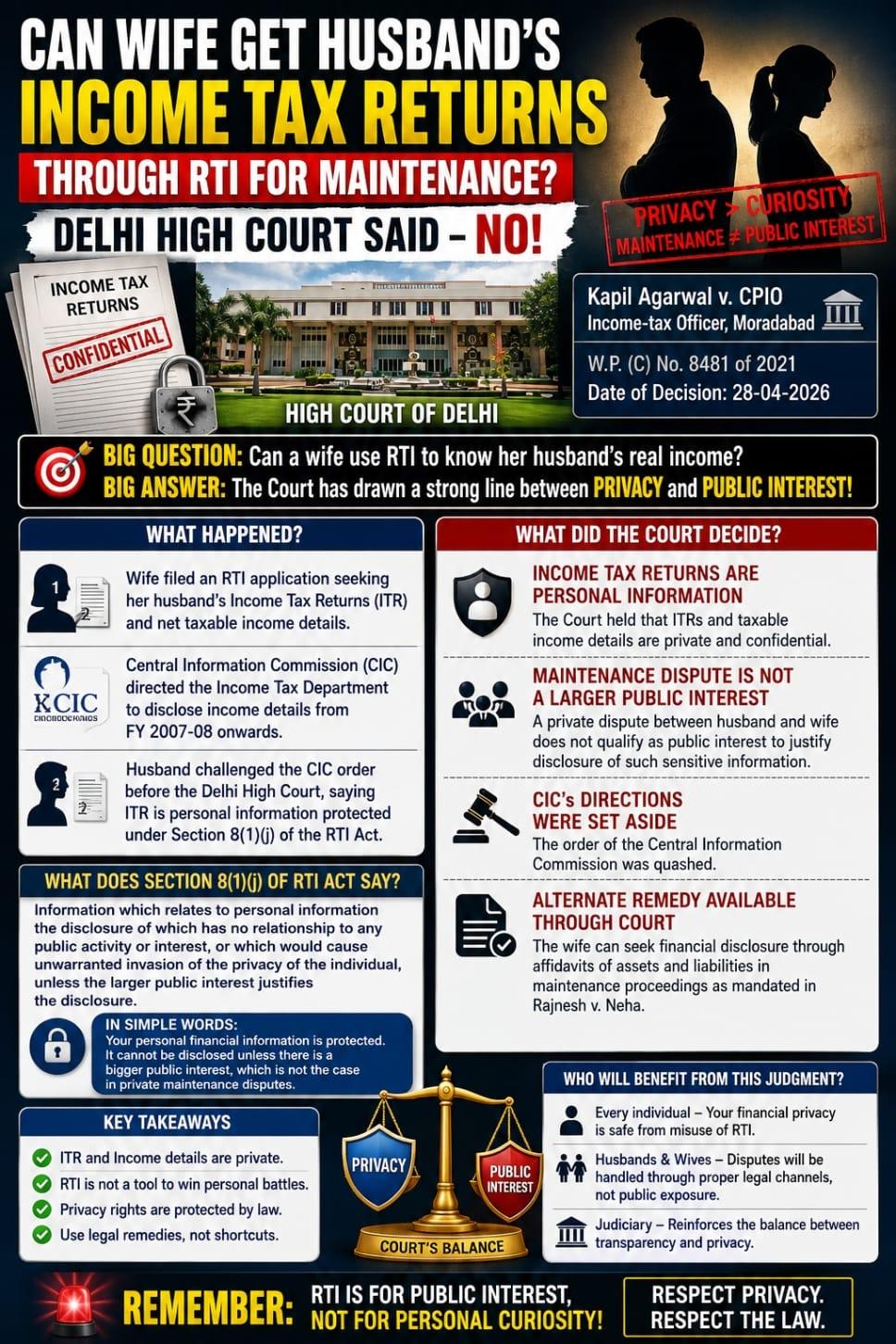

Delhi HC Rules Wife Cannot Seek Husband’s ITR Through RTI in Maintenance Dispute ##

In a major judgment protecting financial privacy, the Delhi High Court has ruled that a wife cannot obtain her husband’s Income Tax Returns (ITR) through the Right to Information (RTI) Act merely for use in a maintenance dispute. The Court held that income-tax returns are personal and confidential information protected under Section 8(1)(j) of the RTI Act.

The case has sparked significant discussion among legal professionals, taxpayers, and matrimonial litigants because it draws a clear line between transparency and an individual’s right to privacy.

Case Details

Case Name:

Kapil Agarwal vs. CPIO Income-tax Officer, Moradabad

Court:

Delhi High Court

Case Number:

W.P. (C) No. 8481 of 2021

Date of Decision:

28 April 2026

Background of the Dispute

The matter arose during pending maintenance proceedings between a husband and wife.

The wife filed an RTI application seeking disclosure of:

- Husband’s Income Tax Returns (ITR)

- Net taxable income

- Financial details from the Income Tax Department

Her objective was to determine the actual income of the husband for claiming maintenance.

CIC Had Allowed Disclosure

Earlier, the Central Information Commission (CIC) directed the Income Tax Department to disclose the husband’s taxable income details from Financial Year 2007-08 onwards.

The CIC believed that such information could help in maintenance proceedings.

However, the husband challenged this direction before the Delhi High Court.

Husband’s Arguments Before the Court

The husband argued that:

- Income Tax Returns are personal and confidential documents.

- Disclosure of ITR details violates the right to privacy.

- Such information is exempt under Section 8(1)(j) of the RTI Act.

- A private matrimonial dispute cannot be treated as “larger public interest.”

What Does Section 8(1)(j) of RTI Act Say? #

Section 8(1)(j) of the RTI Act protects personal information from disclosure if:

- It has no relationship to public activity or public interest, and

- Disclosure would amount to an unwarranted invasion of privacy.

The Court observed that financial records and income-tax returns clearly fall within the category of personal information.

Delhi High Court’s Decision #

The Delhi High Court ruled in favour of the husband and set aside the CIC’s order.

The Court made several important observations:

1. ITR Is Personal Information

The Court held that:

- Income Tax Returns

- Taxable income details

- Financial disclosures made before tax authorities

are confidential personal information protected under the RTI Act.

2. Maintenance Dispute Is Not “Public Interest”

The Court clarified that a maintenance dispute between husband and wife is a private dispute and does not amount to “larger public interest” necessary for disclosure under RTI law.

Therefore, confidential financial information cannot be disclosed merely because matrimonial litigation is pending.

3. Alternative Legal Remedy Is Available

The Court also noted that the wife is not left without remedies.

It referred to the Supreme Court judgment in Rajnesh vs. Neha, under which parties in maintenance proceedings can be directed by courts to file:

- Affidavits of income

- Asset disclosures

- Liability statements

- Financial details

Thus, financial transparency can still be ensured through judicial proceedings instead of RTI applications.

Why This Judgment Is Important #

This judgment is significant because it reinforces the balance between:

✅ Right to Information

✅ Right to Privacy

The ruling makes it clear that RTI cannot be used as a tool to access confidential personal financial data in private disputes.

Key Takeaways #

- Husband’s ITR cannot be obtained through RTI for maintenance cases.

- Income-tax returns are protected personal information.

- Maintenance disputes do not qualify as “larger public interest.”

- Financial disclosures can still be sought through family courts.

- Privacy rights continue to receive strong judicial protection.

Conclusion

The Delhi High Court’s judgment is an important reminder that the RTI Act is intended to promote transparency in public administration, not to expose confidential personal information in private disputes.

While courts can still compel financial disclosure during maintenance proceedings, such disclosure must happen through proper legal mechanisms and not through RTI applications directed at the Income Tax Department. $

Comments (0)

Abhi tak koi comment nahi. Pehle comment karein!